Bank of England Holds Interest Rate at 3.75% – What It Means for You in 2026

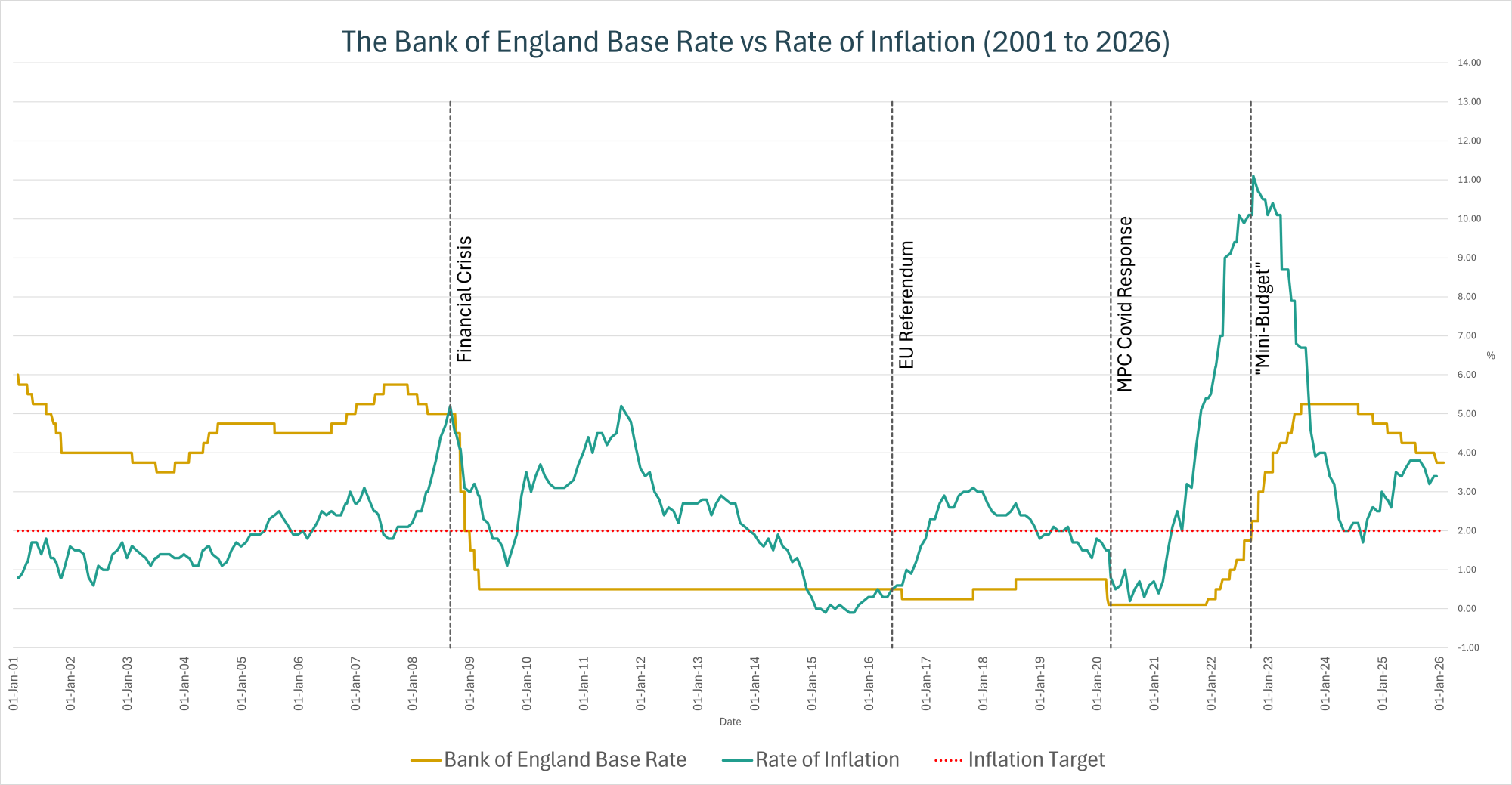

The Bank of England has decided to hold the Base Rate at 3.75% today, following a gradual series of cuts over the past 18 months.

So, what’s going on – and what does it mean for you if you’re thinking about buying a home, remortgaging, or managing your existing mortgage?

Why Is the Base Rate Being Held?

Several key factors influenced the Bank’s decision:

- Inflation has risen – increasing to 3.4% in December, some way above the Bank’s 2% target.

- Economic growth remains fragile – with recent contractions highlighting ongoing pressure on the UK economy.

- The labour market is softening – with rising unemployment and cautious employers.

- Global uncertainty persists – including geopolitical tensions and volatility linked to US trade policy.

In short: while inflation has fallen from the dizzying heights of the recent past, global and economic uncertainty has led the Bank to pause.

What About Future Interest Rate Cuts?

The direction of travel has remained downward since August 2024, when we saw the first of a series of gradual cuts from the Base Rate’s recent peak of 5.25%.

Governor Andrew Bailey has repeatedly indicated that rates are on a “gradual downward path”, provided inflation continues to ease – with pre-credit crisis levels referenced as a realistic long-term target. That said, if the past few years have taught us anything, it’s that economic conditions can change… and quickly.

Recent votes within the Monetary Policy Committee (MPC) have been tight, reflecting differing views on how quickly inflation will return to target.

Financial markets currently expect two further quarter-point cuts during 2026, with the first potentially coming as early as March. However, most economists now believe we are closer to the end of the cutting cycle than the beginning.

That doesn’t mean opportunities aren’t emerging.

How Does This Affect Mortgage Holders and Buyers?

- Fixed-rate mortgage?

Your payments won’t change for now – but falling swap rates are already influencing new mortgage pricing.

If your deal ends in the next 6–12 months, review your options early.

- Tracker or Standard Variable Rate mortgage?

Likely no immediate change – but a cut later in the year could lower your monthly payments.

There are many moving parts – of which the Bank of England Base Rate is just one. With housing stock still limited in many areas and confidence returning, competition remains strong.

If you’ve found the right property at the right price, timing the market perfectly is rarely realistic. Act.

Final Thoughts

We’ve seen huge shifts over the past few years – from historic lows during the pandemic to sharp rate increases in response to inflation, and more recently a carefully managed descent providing some relief for borrowers.

While uncertainty hasn’t disappeared, the outlook for borrowers is far more stable and predictable than it was even 12 -18 months ago.

At Prism, we cut through the noise to help you navigate the ever-changing financial landscape.

As independent, whole-of-market advisers, we continuously monitor lender criteria, pricing, and market conditions to help you make informed, confident decisions – and ensure you secure the most suitable and cost-effective solution for your circumstances and long-term goals.

Whether you’re buying, remortgaging, or simply looking for guidance, get in touch – we’re here to help.

Your Home (or property) may be repossessed if you do not keep up repayments on your mortgage or any other debts secured on it.

Some forms of Buy to Let mortgages are not regulated by the Financial Conduct Authority.

A fee may be charged for mortgage advice. The exact amount will depend on your circumstance.